Stablecoins: The Quiet Takeover

The Digital Dollar Nobody Predicted — And Nobody Can Ignore

Unpegged from Niche

For all its promise, early crypto had a problem: it was nearly impossible to connect to the real world. Traditional banks wanted nothing to do with crypto companies, leaving exchanges and traders without basic banking services - no reliable way to move dollars in, no clean way to move them out. And inside crypto markets themselves, things weren’t much cleaner. Bitcoin, the most trusted asset in the space, was used as the base currency for trading other coins. That sounds logical until you realize it meant every trade carried double the volatility - the asset you were buying was swinging wildly, and so was the currency you were using to buy it. Costs ballooned, positions became nightmares to manage, and the whole ecosystem felt like trying to build a skyscraper on a trampoline. What crypto desperately needed was something boring. Something stable.

That something was the stablecoin - a digital asset pegged to a real-world currency, usually the US dollar. By holding a steady value, stablecoins could do what neither Bitcoin nor traditional banks were willing to do: serve as a reliable bridge. Traders could park profits without cashing out entirely. Exchanges had a neutral quote currency that didn’t gyrate overnight. And crypto businesses finally had a functional unit of account that both sides of a transaction could trust. It wasn’t glamorous, but it was exactly what the ecosystem needed to grow up.

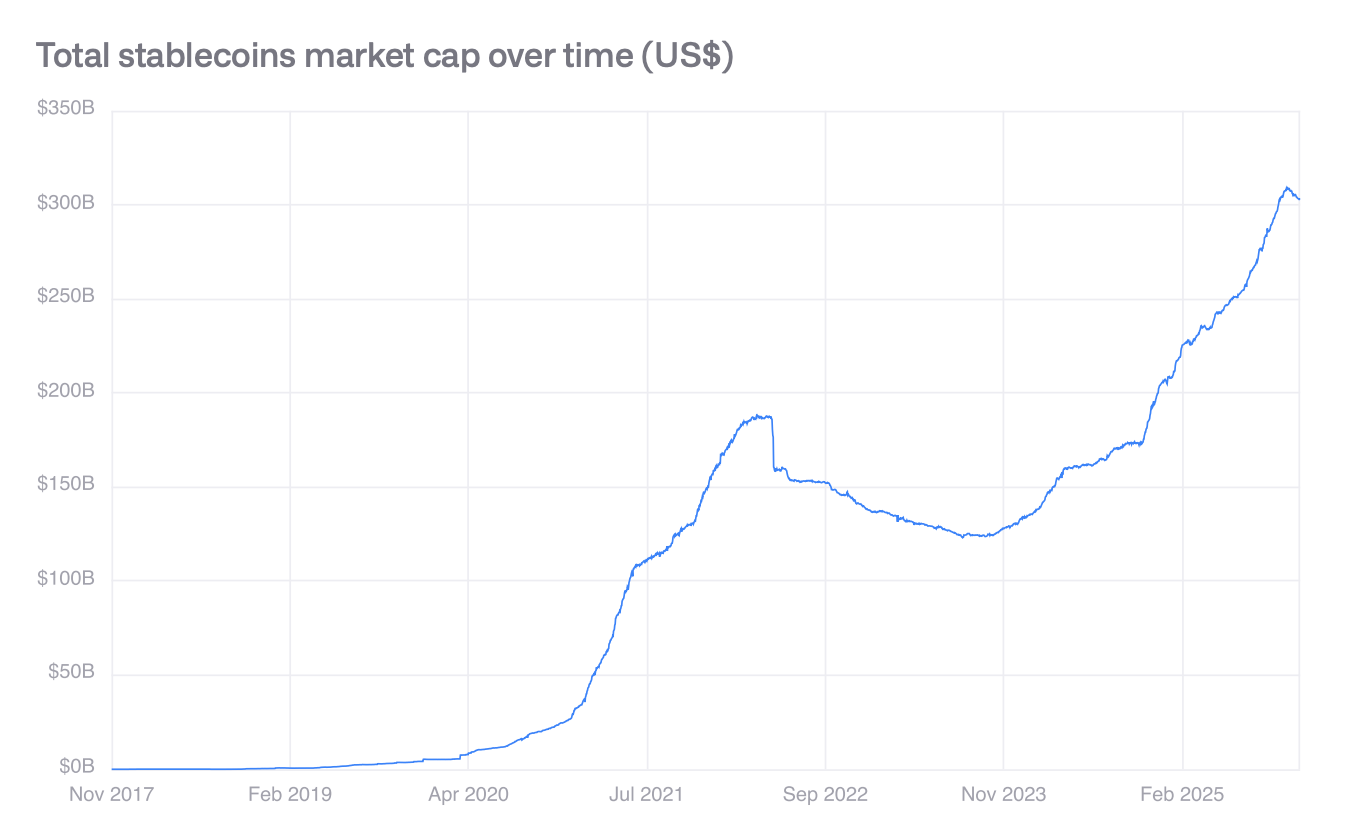

The real stress test came in 2021, when Decentralized Finance (DeFi) exploded into mainstream awareness. Suddenly, stablecoins weren’t just a convenience; they were the backbone of an entirely new financial system. Lending protocols let users deposit volatile crypto as collateral and borrow stablecoins against it, unlocking liquidity without forcing anyone to sell their holdings. Stablecoins also helped reduce impermanent loss, the risk that comes from providing liquidity in pools where asset prices diverge, by anchoring one side of the equation. The numbers tell the story plainly: the stablecoin market grew from $5 billion in 2020 to over $200 billion by 2025. In five years, a niche utility token had become the reserve currency of a parallel financial universe.

Settled in Stablecoins

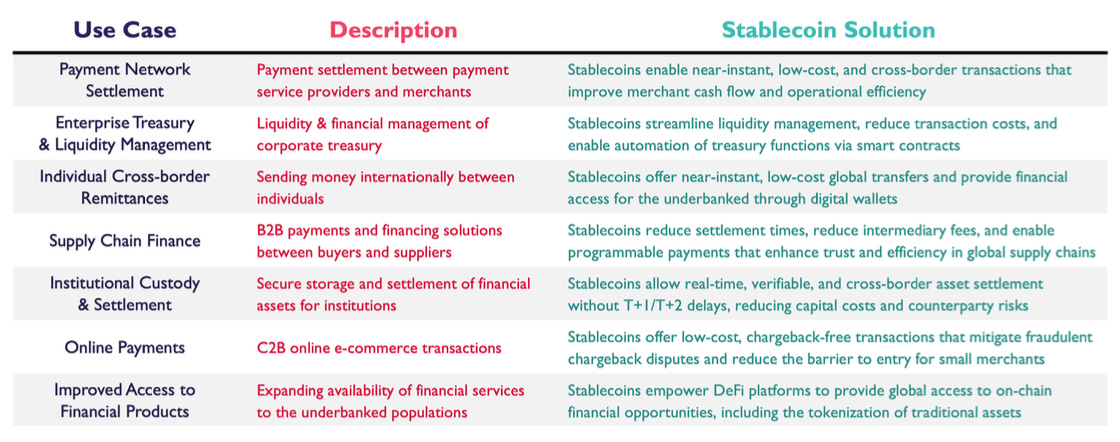

What started as plumbing for crypto traders has since evolved into a full-stack financial infrastructure — one that is now being taken seriously by enterprises, institutions, and governments alike. The use cases have grown far beyond trading. Today, stablecoins power payment settlement between merchants and service providers, enable near-instant cross-border remittances for individuals, and streamline treasury and liquidity management for corporations through smart contract automation. In supply chains, they cut settlement times and eliminate intermediary fees between global buyers and suppliers. For institutions, they remove the friction of settlement delays, reducing both capital costs and counterparty risk. And for the hundreds of millions of people without access to traditional banking, stablecoins, accessible through a simple digital wallet, represent a genuine on-ramp to financial services that were never built for them.

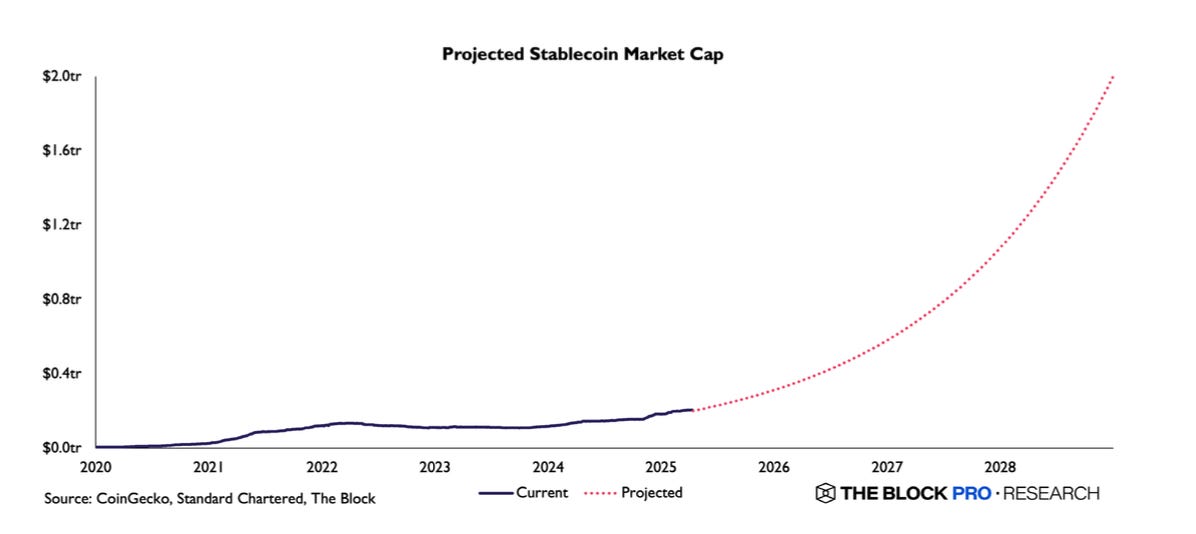

The numbers reflect this expanding role. The stablecoin market grew from under $10 billion in 2020 to over $200 billion by 2025 - and projections from Standard Chartered and The Block suggest the market could approach $2 trillion by 2028. That is not speculative hype; it is the market pricing in the reality that stablecoins are becoming core infrastructure for global payments, DeFi lending, and digital asset settlement. The trajectory on the chart is less a prediction and more a recognition that once a better rail exists, capital tends to flow toward it.

What makes stablecoins genuinely significant is that their most important users may not be crypto-native at all. In high-inflation economies, people are using dollar-pegged stablecoins to protect their savings. Online merchants are adopting them to eliminate chargeback fraud. Multinationals are exploring them to move treasury liquidity across borders without the cost and delay of correspondent banking. The stablecoin, in short, is no longer just a crypto tool - it is quietly becoming one of the most versatile and consequential financial instruments of the decade.

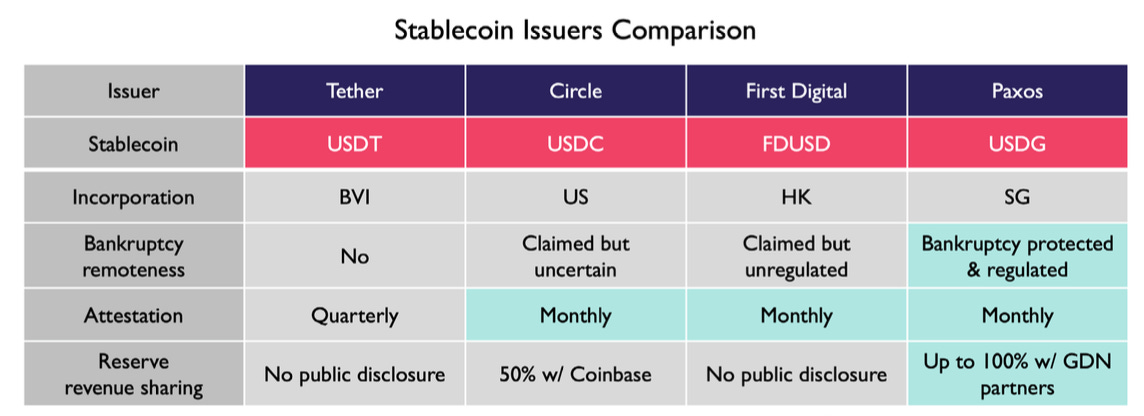

Same Peg, Very Different Players

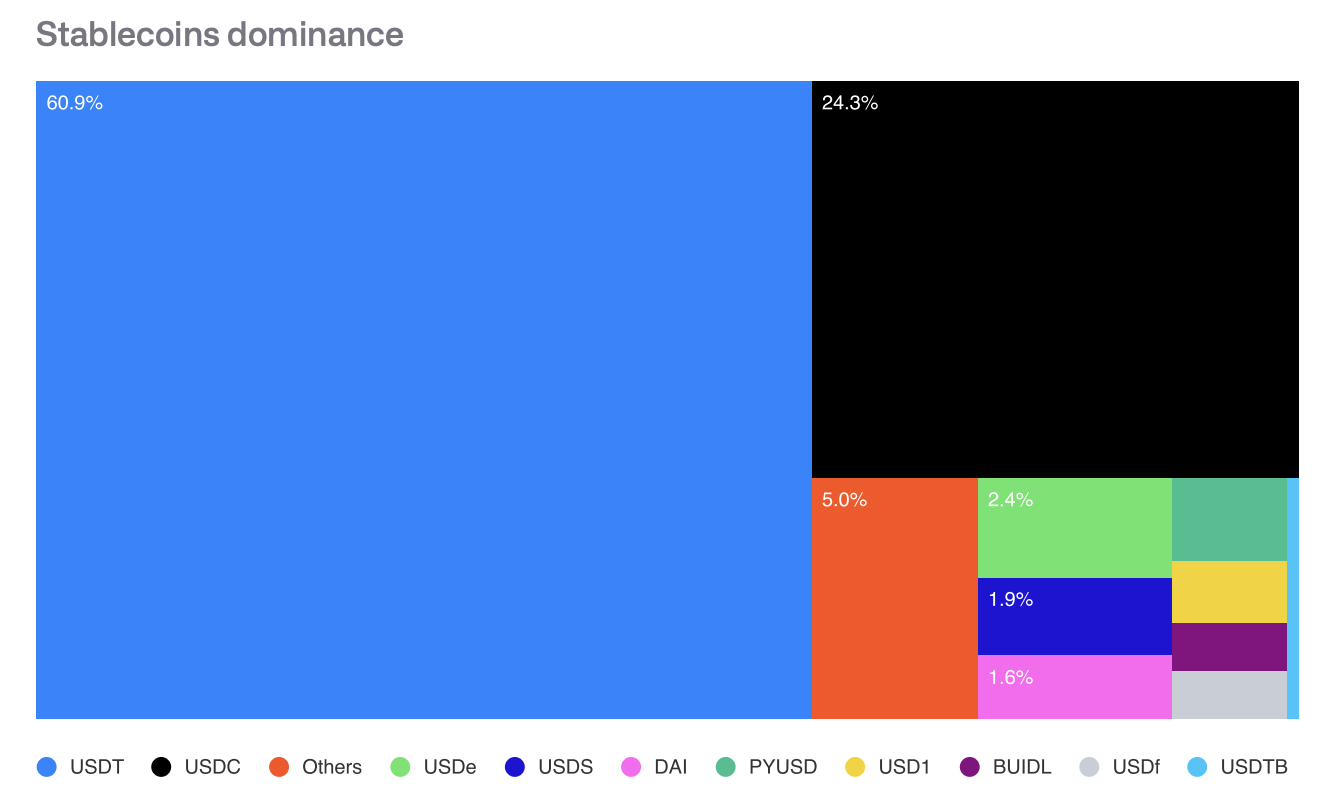

Though all are pegged to the US dollar, not all stablecoins are created equal. Tether (USDT) commands the largest market share with approximately $185 billion in circulating supply, making it by far the dominant force in the stablecoin market. Its nearest competitor, Circle’s USD Coin (USDC), holds a distant second place with roughly $75 billion in circulating supply - less than half of Tether’s footprint. Despite growing regulatory scrutiny and competition from emerging stablecoin issuers, Tether’s dominance remains largely unchallenged, cementing its position as the de facto liquidity backbone of the broader cryptocurrency ecosystem.

Law Meets the Ledger

United States - GENIUS Act

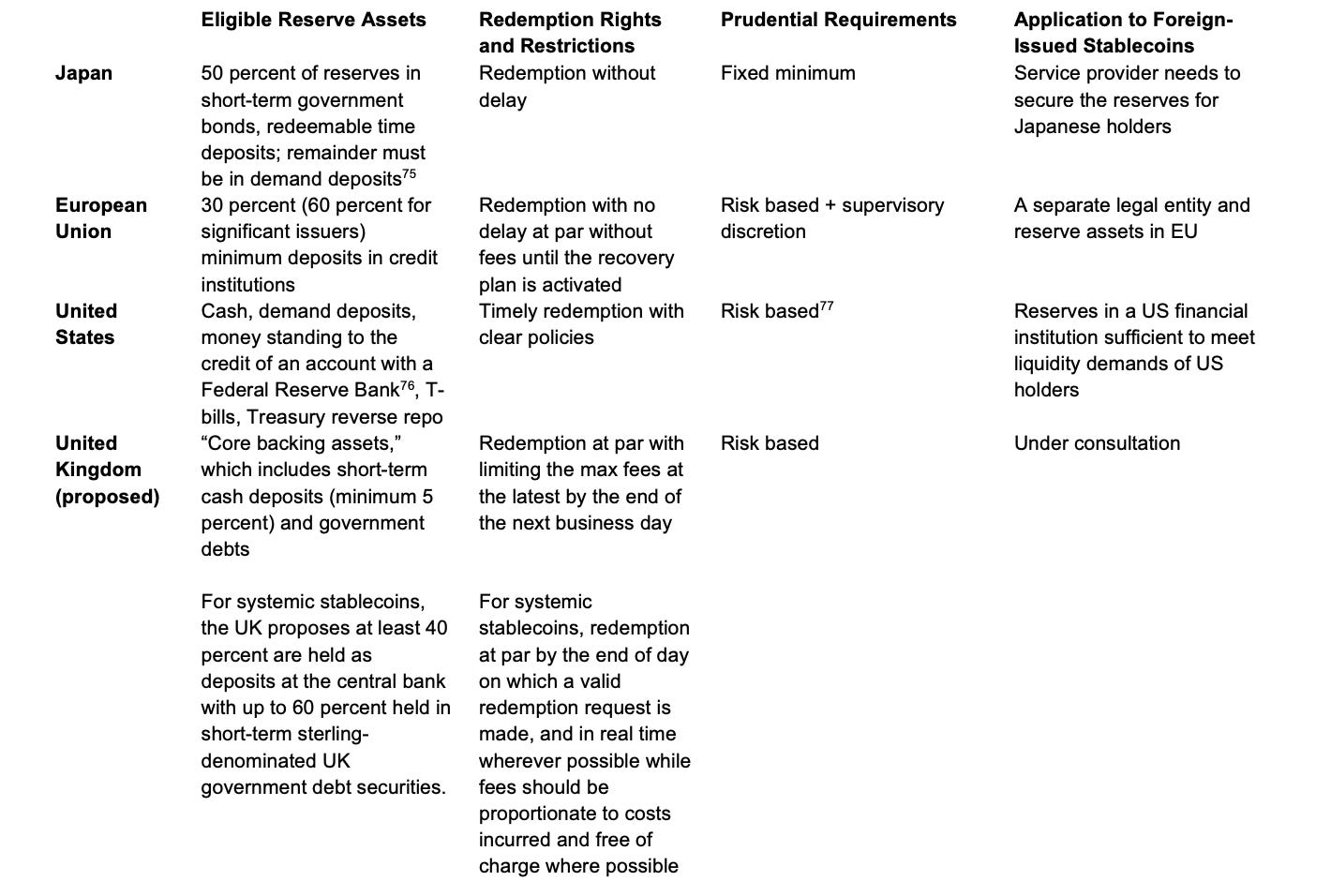

Throughout 2025, the United States regained momentum as political sentiment shifted toward enabling domestic crypto innovation. Regulatory fragmentation, however, remained a drag, with oversight still split across the SEC, CFTC, Federal Reserve, OCC, FDIC, and state regimes, leaving token classification and market-structure rules inconsistently applied.

The landmark development of the year 2025 was the GENIUS Act, signed into law by President Trump on July 18, 2025 which is the first major piece of federal digital asset legislation in US history. The Act established clear reserve requirements for stablecoin issuers, mandated monthly disclosures, and removed compliant stablecoins from SEC and CFTC jurisdiction. While a meaningful step forward, broader regulatory gaps persist.

European Union - MiCA

Europe entered 2025 with MiCA (Markets in Crypto-Assets Regulation) fully in force, establishing the world’s most comprehensive legal framework for crypto-asset issuance, custody, trading, and stablecoins. For institutions, this offered something no other jurisdiction could match: legal certainty across the entire value chain. MiCA’s alignment with existing financial regulation made it naturally compatible with institutional processes, while its stringent reserve and governance standards positioned Europe as the safest environment globally for stablecoin issuance. Under MiCA, a crypto firm licensed in one EU Member State automatically gains the right to operate across all 27 EU countries. However, 2025 also exposed early friction, with several national regulators, including France’s AMF and Italy’s CONSOB, signalling concerns over inconsistent supervisory standards across Member States. Regulators like the AMF and CONSOB signalled they may not simply accept a passport from certain Member States at face value and that they may apply additional scrutiny to firms passporting in from jurisdictions they consider to have weaker oversight. This effectively turns the passport from an automatic right into something a firm still needs to earn through credibility, undermining one of MiCA’s core promises of seamless cross-border operation within the EU. Nonetheless, Europe enters 2026 as the global reference point for structured, institutionally aligned digital-asset regulation.

United Kingdom

The UK has yet to establish a dedicated stablecoin regulatory framework. Throughout 2025, progress remained largely consultative, with HM (His Majesty’s Treasury) Treasury and the FCA (Financial Conduct Authority) publishing discussion papers but stopping short of binding rules. Stablecoins are expected to fall under the upcoming CASP(Crypto Asset Service Provider) licensing framework, though this remains scheduled for late 2025 into 2026, leaving firms operating under temporary exemptions in the meantime. The UK’s approach is broadly expected to mirror MiCA in outcomes, but meaningful regulatory clarity for stablecoin issuers remains a 2026 and beyond story.

Asia

Stablecoin regulation across Asia in 2025 remained fragmented but moving in the right direction. Hong Kong led the way, advancing a dedicated licensing regime for stablecoin issuers with clear reserve, governance, and disclosure requirements. Singapore followed a similar path under its Payment Services Act, requiring issuers to hold full reserves in high-quality liquid assets alongside strict AML(Anti-Money Laundering) obligations.

Japan introduced its stablecoin framework in 2022, which came into effect in 2023, making it one of the first countries in the world to pass dedicated stablecoin legislation. The framework established a few key rules:

Only licensed banks, registered money transfer agents, and trust companies are permitted to issue stablecoins — effectively restricting issuance to regulated financial institutions.

Stablecoins must be pegged to the Japanese Yen or another legal tender and fully redeemable at face value, meaning holders can always exchange their stablecoin for the equivalent in cash.

Issuers are required to hold reserves in a way that protects customers, with strict rules around custody and segregation of assets.

In practice, this made Japan’s framework quite conservative prioritising stability and consumer protection over openness. Japan remained more cautious, continuing to refine rules around custody and reserve transparency without major new developments.

Further afield, South Korea remained focused primarily on consumer protection rather than building out a comprehensive stablecoin framework. While Asia as a whole is gradually converging toward reserve-backed, bank-aligned stablecoin standards, the regulatory experience still varies significantly by jurisdiction.

A Portfolio Perspective

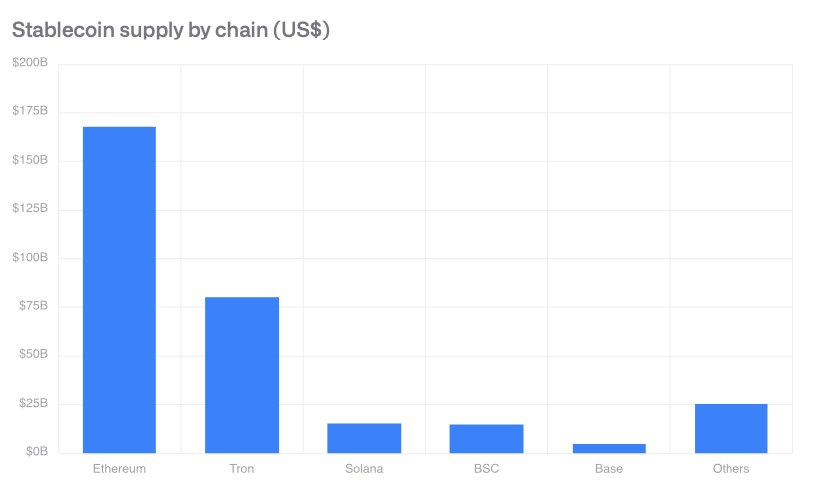

Public blockchains that support smart contracts such as Ethereum, Solana, and various Ethereum Layer-2 networks serve as the foundational infrastructure for the gradual fusion of decentralised technology with traditional finance. These networks host nearly all decentralised applications and are essential for processing stablecoin transfers, tokenised asset settlements, and decentralised exchange activity, generating approximately $7 billion in fees during 2024 alone, with Ethereum and Solana accounting for more than half of that revenue.

Stablecoins represent one of the most significant use cases for these networks. The stablecoin market now exceeds $300 billion in total supply, with Ethereum commanding the largest share and Solana experiencing the fastest growth. Given the central role these blockchains play in the evolving financial infrastructure, gaining exposure to assets like Ethereum and Solana — through vehicles such as the BGCI Product or the BitSave Crypto & Gold product— represents a compelling portfolio consideration.