The Great Unlocking: How Tokenisation Is Rewriting the Rules of Asset Ownership

From property to gold to government bonds: how blockchain is quietly rewiring the infrastructure of ownership

What is tokenisation?

Tokenisation is the process of taking a real world asset, something like a building, a government bond, a piece of private credit, or even a commodity, and representing ownership of it as a digital token on a blockchain. Think of it as giving a physical or financial asset a digital passport that can be traded, split into smaller pieces, and settled almost instantly. What once took days of paperwork and middlemen can now happen in seconds, with every transaction recorded on an immutable ledger that anyone can verify. The appeal is obvious: it makes assets that were historically locked up and illiquid feel almost as easy to move as transferring money between two bank accounts.

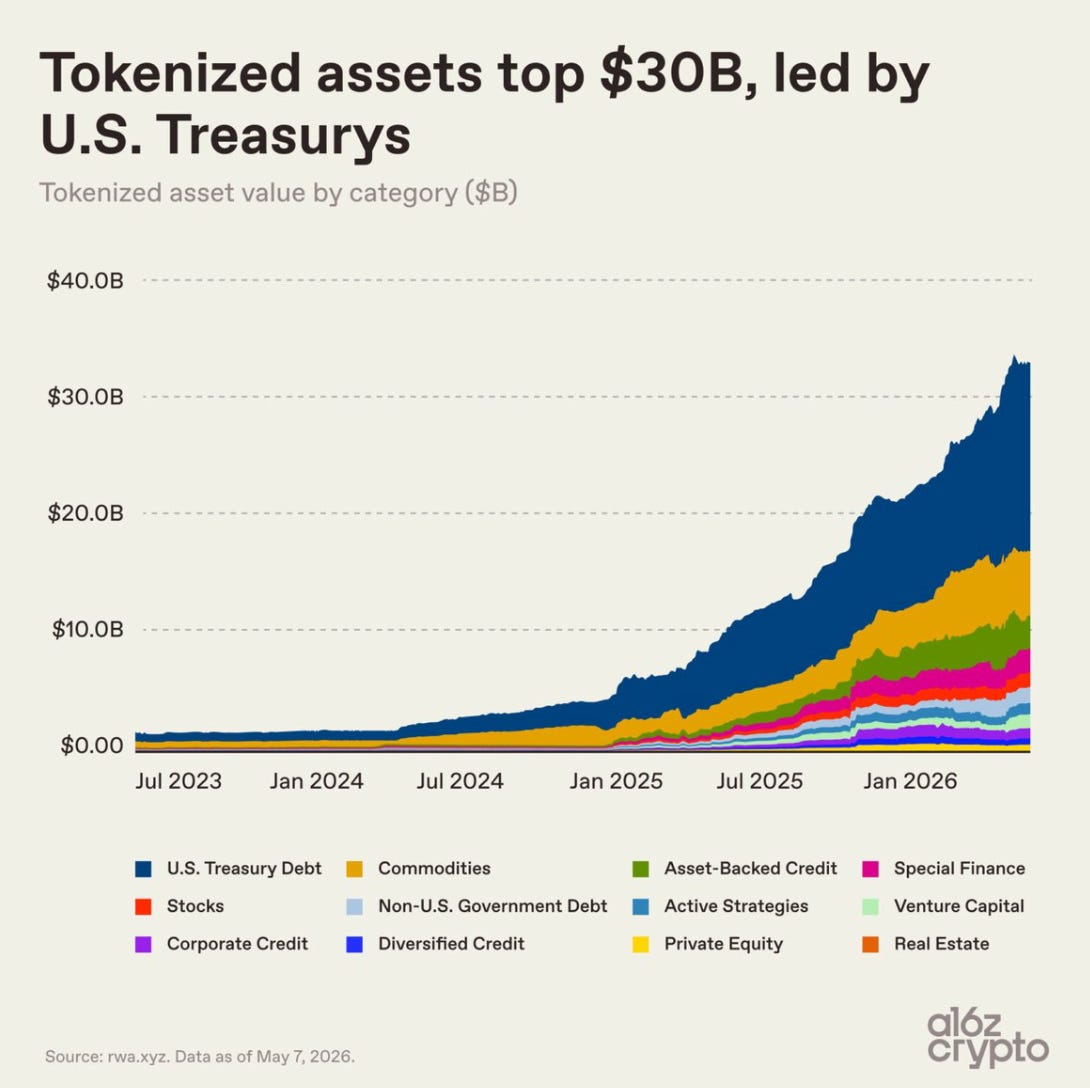

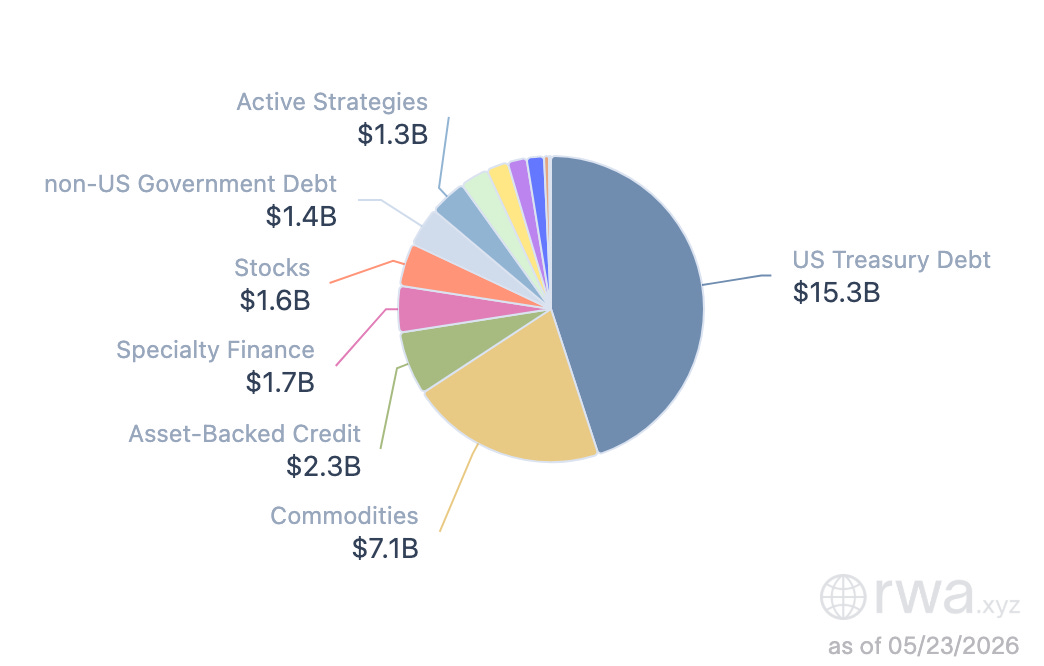

The growth over the last two years has been genuinely startling. Tokenised real world assets have climbed to over $34 billion in total value as of May 2026, up from around $5.5 billion at the end of 2024, representing growth of roughly 229% through 2025 alone. Tokenised US Treasuries have led the charge, now accounting for over $15 billion of that total. This is not retail enthusiasm driving things either. Asset managers, family offices, and institutional investors are now actively building tokenised product lines, drawn by real yield, faster settlement, and the ability to reach a much broader investor base than traditional finance ever allowed.

What has changed most recently is not just the money flowing in but the conditions making it sustainable. The GENIUS Act in 2025 established the first federal regulatory framework for stablecoins, requiring full reserves and monthly disclosures, while the Clarity Act working through Congress is expected to clarify how digital assets sit alongside securities and commodities. For years, institutions sat on the sidelines waiting for exactly this kind of regulatory plumbing. Now that it is arriving, the longer term projections are becoming bolder. McKinsey estimates the market could reach $2 trillion by 2030 under conservative assumptions, while more optimistic forecasts put it closer to $30 trillion. Whether reality lands closer to the cautious or the bullish end, the direction is no longer in doubt.

Why Tokenisation, Why Now

For most of financial history, the value of an asset and the ease of owning it have been two separate things. A commercial real estate building in Mumbai or a Japanese government bond might be perfectly sound investments, but accessing them, transferring them, or using them as collateral has always involved layers of intermediaries, jurisdiction-specific paperwork, and settlement cycles measured in days rather than minutes. The infrastructure around the asset has always been the harder problem.

Tokenisation is one answer to that problem, and it has been discussed as such for nearly a decade. What is different now is that institutions which do not move speculatively are building on this infrastructure in earnest. Several structural advantages explain the pull.

1. Fractional ownership and broader access. Tokenisation allows large assets to be divided into smaller units, lowering minimum investment sizes and widening participation across both capital thresholds and geographies. Investors can spread capital across multiple assets rather than commit to a single large position, and issuers can access a broader investor base without depending on traditional distribution networks.

2. Improved liquidity. Many real-world assets are difficult to trade in conventional markets. Tokenisation can improve liquidity by making ownership interests easier to transfer and by reducing the size of the stake that needs to change hands in each transaction.

3. Lower transaction costs and faster settlement. Traditional transfers often involve several intermediaries, manual checks, and delayed reconciliation. Tokenised systems can reduce that friction by placing issuance, transfer, and record-keeping on shared digital infrastructure, lowering costs while shortening settlement times.

4. Transparency. Tokenised assets create clearer records of ownership and transaction history, which improves traceability. That same visibility supports stronger compliance controls, transfer restrictions, and reporting functions, making tokenised structures easier to monitor within regulated market settings.

5. Programmability. Once assets are represented as tokens, they can be linked to automated functions such as distributions, collateral use, permissions, and compliance checks. This gives tokenised assets a degree of operational flexibility that conventional formats usually lack.

Taken together, these advantages change the underlying architecture of how assets are issued, held, and transferred. That is the scale of change now underway.

How to Tokenise

Tokenisation begins with a simple question: what exactly is being turned into a token? In the case of a solar project, for example, the token may represent ownership in the project, a share of future cash flows, or a claim on the revenue generated from electricity sales. The rights attached to the token have to be defined clearly at the outset, because the digital token is only as strong as the legal and economic claim behind it.

Take a solar project in Rajasthan valued at INR 20 crore. Instead of financing the entire project through one large investor or a small group of institutions, the project can be placed inside a legal structure and divided into 2,00,000 tokens. In that case, each token represents INR 1,000 of economic exposure to the project. If the project generates monthly revenue from power sales, that income can then be distributed proportionally to token holders.

Once issued, those tokens can also be transferred or traded, meaning an investor who wants to exit does not need to wait for the project to conclude or find a buyer for the entire position. This is the basic logic behind tokenisation: turning a concentrated, illiquid claim into a smaller, more transferable one.

1. Define the asset and the claim. The first step is to decide what the token will represent. In a solar project, this could be direct ownership, a revenue share, or a claim on project cash flows.

2. Set up the project structure. The asset is usually held through a special purpose vehicle, trust, or similar arrangement. This is what connects the token to a real, enforceable interest in the project.

3. Link the project data. The token needs a reliable link to the underlying asset, whether through production data, revenue records, reserve accounts, or other verification mechanisms. Without this link, the token exists only as a digital entry, whether the underlying asset is a solar project, a property, or a bond.

4. Mint and programme the token on-chain. Once the structure is in place, the token is created on blockchain and encoded with its operating rules, covering transfer restrictions, payout rights, investor eligibility, and reporting requirements.

5. Issue the token to investors. The token is offered through a primary issuance or approved placement process. Investors hold it digitally rather than through a conventional custody structure.

6. Manage payouts and reporting. The token supports ongoing distributions, record-keeping, and where relevant, redemption or exit mechanics. In a solar project, this means investors receive their share of revenues as the project generates income over time.

Each step carries the weight of the others. The legal right, the economic exposure, and the digital token stay connected and usable in the market only when the full structure holds.

The Risks and Challenges of Tokenisation

Tokenisation makes assets easier to access and transfer, but it also introduces a second layer of dependence: the token relies on both the off-chain foundation and the on-chain infrastructure. If either break, the claim behind the token may be difficult to enforce.

1. Legal and regulatory uncertainty. Tokenised assets do not fit neatly into one legal category. In some jurisdictions they may be treated as securities, in others as commodities, payment instruments, or something else entirely. Cross-border issuance and trading add further complexity because rules on ownership, transfer, tax, and investor eligibility differ from market to market.

2. Ownership, enforceability, and custody. Holding a token does not automatically guarantee legal title to the underlying asset. Its strength depends on whether it is tied to a recognised legal claim that can be enforced in the event of a dispute, insolvency, or transfer problem. The underlying asset must be held and verified off-chain, which introduces dependence on outside parties.

3. Smart contract and data risk. Tokenised systems rely on external data feeds and code. If the data is inaccurate or the smart contract is flawed, the consequences can include frozen transfers, loss of funds, or outcomes that are difficult to reverse.

4. Fragmentation. Tokenised assets currently sit across different blockchains and legal structures that do not always communicate with each other. Until interoperability improves, that limits the practical utility of tokenisation at scale.

5. Governance and compliance. Tokenised structures still need to meet KYC, AML, and disclosure requirements, and gaps in those controls create regulatory exposure. Where governance is unclear, investors may face uncertainty over who controls the rules, who can change them, and what recourse exists if something goes wrong.

Recognising these risks is the starting point. How well they are managed will determine whether tokenisation delivers on its structural promise or remains a fragile overlay on conventional finance.

Regulation

United States

The United States currently has no single regulator or law dedicated to tokenised assets. Instead, multiple federal and state agencies each claim jurisdiction depending on how a token is structured, creating a fragmented, often unpredictable compliance landscape for issuers and institutions alike.

The CLARITY Act aims to change that. The bill passed the US House of Representatives in July 2025 with a strong bipartisan vote of 294-134. Most recently, the Senate Banking Committee advanced it on May 14, 2026, a significant milestone, though the bill still needs to clear a full Senate vote and receive a presidential signature before becoming law.

At its core, the CLARITY Act proposes sorting all crypto assets into three distinct buckets: digital commodities, investment contract assets, and permitted payment stablecoins. Each category would fall under a defined regulatory authority, primarily the CFTC or the SEC, based on the token’s characteristics.

This matters enormously for tokenisation. Today, whether a token is a security or a commodity often comes down to enforcement actions and court rulings rather than clear statutory rules. The CLARITY Act would replace that guesswork with codified criteria. A token representing ownership in real estate or private equity would fall under SEC oversight; one backed by a physical commodity would likely land with the CFTC. The practical effect is that token issuers would know upfront which rules apply to them and can build accordingly.

European Union

The EU has taken one of the more structured approaches to crypto regulation with the introduction of MiCA (Markets in Crypto-Assets Regulation), which rolled out in stages through 2024-2025. But for real-world asset tokens specifically, the framework isn't as simple as one rulebook. The key question regulators ask is: does this token behave like a stock or a bond? If it gives holders profit shares, voting rights, or ownership in an underlying asset, it gets treated like a traditional security, falling under older financial laws like MiFID II, with all the compliance weight that carries. If it simply tracks the value of an asset like gold or real estate without promising returns, it lands under MiCA instead, typically classified as an Asset-Referenced Token (ART).

Gulf

The Gulf region has quietly become one of the more interesting places to watch when it comes to real-world asset tokenisation, and the UAE is leading the charge. Dubai’s Virtual Assets Regulatory Authority (VARA) has built what is arguably the most comprehensive legal framework for RWA tokens anywhere in the world. With its 2025 Rulebook update, Dubai formally legalised the issuance, listing, and trading of tokenised real-world assets, classifying them as Asset-Referenced Virtual Assets (ARVAs). Issuers face full disclosure requirements, whitepaper obligations, and reserve rules.

The Dubai Land Department’s first tokenised real estate project, launched through the Prypco Mint platform in May 2025, sold out within a single day of going live. The offering attracted 224 investors spanning 44 nationalities, with 70% entering Dubai’s real estate market for the first time, a sign that fractional ownership is genuinely opening the asset class to new capital. With a minimum investment of just AED 2,000, an average ticket size of AED 10,714, and a waitlist already exceeding 6,000 requests, the demand signal was hard to ignore.

Beyond the UAE, the picture varies widely. Bahrain has moved quickly, building out licensing frameworks and launching formal stablecoin rules in 2025. Saudi Arabia is still catching up. Crypto sits under AML laws for now, with a proper licensing regime expected soon. Qatar, which banned crypto as recently as 2020, is gradually opening up through its Qatar Financial Centre. Kuwait remains the most restrictive, with a broad ban still in place. What ties the region together is a clear ambition to compete for tokenisation business, particularly in the UAE, where Dubai and Abu Dhabi are almost racing each other to attract Web3 projects. For RWA issuers, the Gulf is no longer just an emerging market to watch. It’s becoming a serious destination.

Asia

Asia has emerged as one of the most active regions for RWA tokenisation, with Singapore and Hong Kong leading the way. Both cities have built more structured regulatory environments than most other financial centres, offering clarity that actively encourages institutional participation. The Monetary Authority of Singapore (MAS) has been running Project Guardian, a public-private collaboration testing tokenisation models under regulatory supervision, which by 2025 had tested over 15 tokenised asset trials across bonds, real estate, and six currencies. Hong Kong, meanwhile, accelerated its digital asset strategy in 2025, advancing its licensing regime, expanding live settlement infrastructure, and launching the HKMA’s Project Ensemble sandbox to test tokenisation use cases locally and across the region.

Japan and other Asian markets are moving more gradually but in the same direction. Japan amended its Payment Services Act to provide a structured path for digital securities, while South Korea and Thailand explored tokenisation in investment products. The broader regional approach differs from the EU’s in one notable way. Rather than building a single unified rulebook, Asian regulators are largely competing with each other to attract projects, while quietly converging on similar standards.

A final note

Tokenisation is no longer a concept waiting for its moment. The infrastructure is arriving. Regulatory frameworks are live across the EU, UAE, and Singapore, institutional capital is moving in earnest, and the market has grown from $5.5 billion to over $34 billion in under eighteen months. The risks around legal enforceability, smart contract failure, and cross-chain fragmentation are real and will take time to resolve, but they are engineering problems, not fundamental objections. What the Dubai Land Department’s sold-out token offering, BlackRock’s tokenised fund, and the CLARITY Act’s Senate progress all point to is the same thing: the plumbing is being built, and capital is following. The only remaining question is the pace.